The last ice age lasted a very long time and caused a significant regression in the biological advance of life on earth.

I think we are on the verge of entering into a new kind of ice age — an economic one — around the world today.

Massive debt loads weigh down the economy in every sector, forcing central banks to fight tooth and nail to keep interest rates low.

Meanwhile, demographic researchers recently posited that the peak of human population on the planet is coming much sooner than previously expected and will decline rapidly afterward.

Though GDP growth should remain sluggish, at best, some asset classes should perform well in an "economic ice age" environment.

Looking for a helping hand in the market? Members of High Yield Landlord get exclusive ideas and guidance to navigate any climate. Get started today »

The last ice age lasted a very long time and caused a significant regression in the biological advance of life on earth.

I think we are on the verge of entering into a new kind of ice age — an economic one — around the world today.

Massive debt loads weigh down the economy in every sector, forcing central banks to fight tooth and nail to keep interest rates low.

Meanwhile, demographic researchers recently posited that the peak of human population on the planet is coming much sooner than previously expected and will decline rapidly afterward.

Though GDP growth should remain sluggish, at best, some asset classes should perform well in an "economic ice age" environment.

Looking for a helping hand in the market? Members of High Yield Landlord get exclusive ideas and guidance to navigate any climate. Get started today »

Ice Ages, Old And New

The last ice age ended around 14,000 years ago, according to the geological consensus, during the Pleistocene Epoch. It lasted a long, long time. In fact, some remnants of the last ice age remain today. Glaciers in Greenland and Antarctica have been slowly receding since the Pleistocene era.

During an ice age, glacial ice sheets advance from the poles toward the equator, never covering the entire planet. Actually, the glaciers were constantly in flux, advancing and receding and advancing and receding, although that flux would barely be noticeable in a human lifetime.

During an ice age, the earth overall was much colder and drier. Variations in the weather sometimes caused the ice to advance faster than many species could adapt or move, and many went extinct because of it. Around three-fourths of all large animal species (mainly vertebrate mammals) completely died out during this period.

Saber-toothed tigers, mastodons, and woolly mammoths are examples. Much plant life also perished, even in areas that weren't covered in ice. Whole forests were consumed by the glacial advance. Entire ecosystems disappeared. The biological progression of life was put on pause, or even reversed, during this cold, dour period.

But scientists also believe that it was the Pleistocene ice age that formed humans into basically the creatures we are today. As migratory herds of animals moved toward the warmer parts of the earth around the equator, humans followed. Over many generations, these hunter-gatherer bands developed tools and complex clothing and learned to survive wherever they went. They were forced by a harsh environment to become smarter and more advanced.

You may already see where I'm going with this metaphor. For multiple reasons, I believe the global economy is now entering what I think of as an "economic ice age."

Just as the ice age of history caused a long pause or even contraction in the biological progression of life on earth, I think the "ice age" we are entering will cause a long pause or even contraction in humanity's economic progression. For a long time to come, our standards of living will rise at a crawling pace or perhaps even remain flat. Innovation will be incremental and concentrated in certain areas rather than the widespread leaps and bounds of advancement enjoyed over the 20th century.

There are several factors at play in the global economy today that bring me to this view, even while I remain optimistic about certain asset classes going forward. In this first installment, I want to discuss two of the biggest tectonic forces at play in the economic world today and finish with three predictions.

Just like the humans of the last ice age, we investors will need to become smarter and more adaptive in the years and decades to come.

Interest rates are sitting at zero, making credit cheaper. Cheaper credit spurs ballooning debt, even while investors around the world are desperate to find yield, thus keeping yields and interest rates low. But more debt, especially when it is taken out to fund consumption rather than productive investment, cripples the economy's ability to expand.

I've written about this on many occasions in the past. (See, for instance, "The Monetary Death Spiral.") There are basically three ways to pay for government spending: tax revenue, debt issuance, or money printing (which is inherently inflationary). All else being equal, fiscal deficits soak up domestic private savings, which reduces economic growth by crowding out private investment. But it can also be funded through increased trade deficits: Foreigners give us goods, we give them dollars, and they buy our government debt.

It's easy to see how this forms a self-reinforcing cycle: more debt leads to lower growth leads to more debt leads to lower growth. This leads to the inability of central banks to let rates rise, because in a highly indebted economy, even a small rise in rates causes debt service costs to soar.

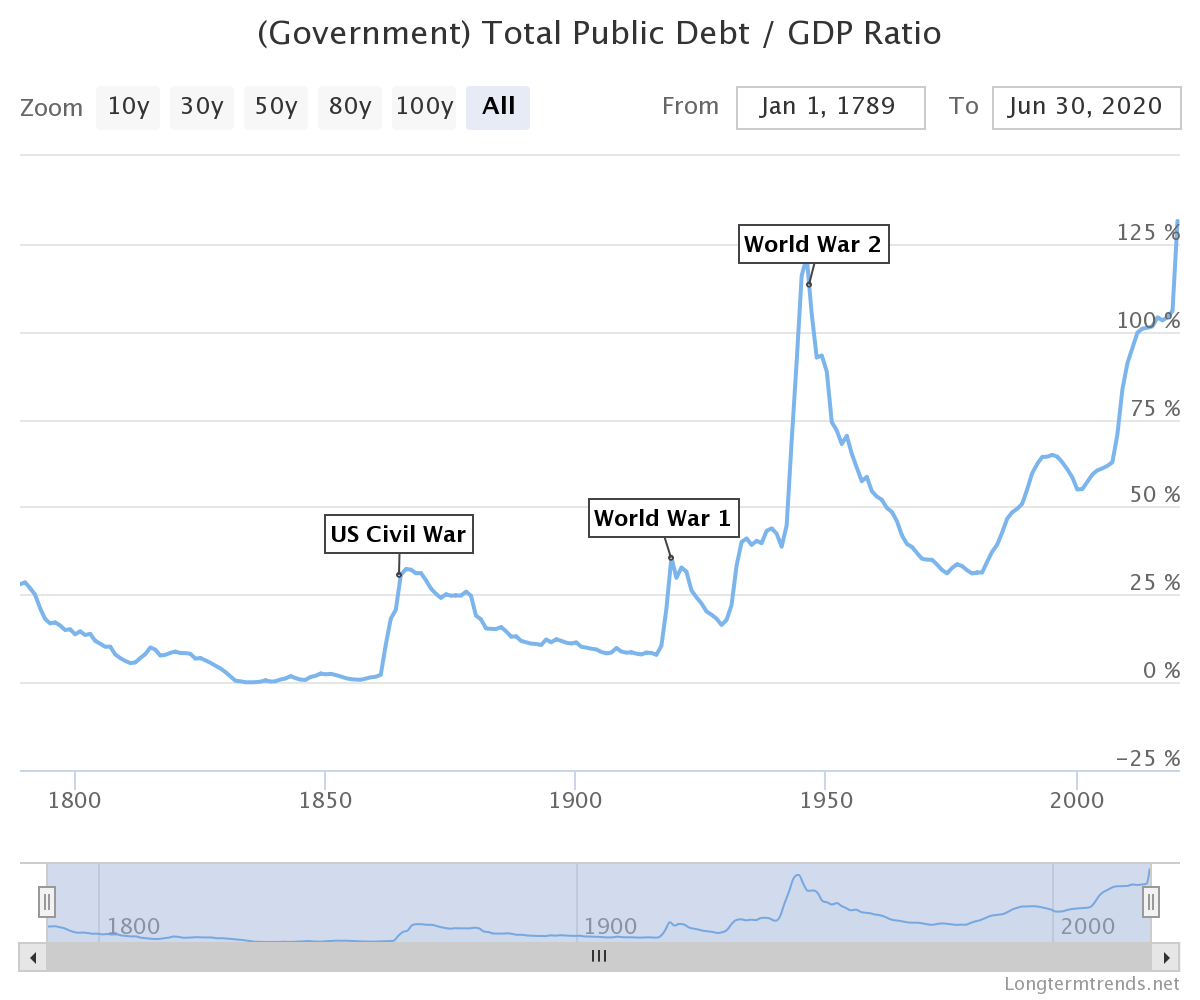

As we can see in the chart below, federal government debt to GDP is now higher than at any time in our nation's history, including the peak of World War II.

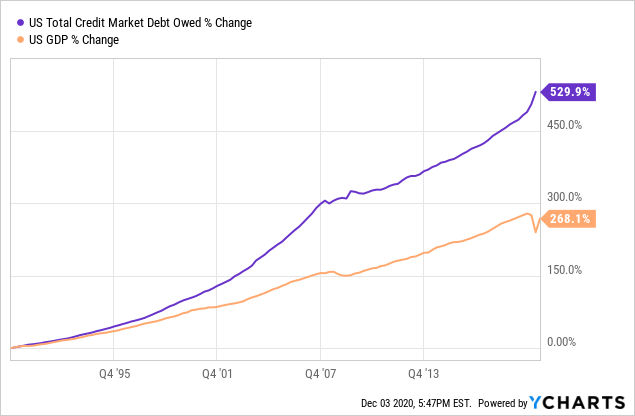

Zooming in to the period from 1990 to today, we find that total credit market (public and private) debt has increased at roughly double the rate of GDP:

In my view, the persistent focus from policymakers on increasing consumption, even at the expense of a higher debt load, is short-sighted. It isn't that more government spending and stimulus can't produce temporary bursts of growth or fill the chasm in consumption caused by the pandemic. It can.

But there are two problems. First, such spending necessarily must come from either taxes (private sector income), debt (private savings), or an increased trade deficit (foreign investors that cannot be relied on permanently). Money printing is not legally an option for the government at this point. Second, it misunderstands how economies grow over time.

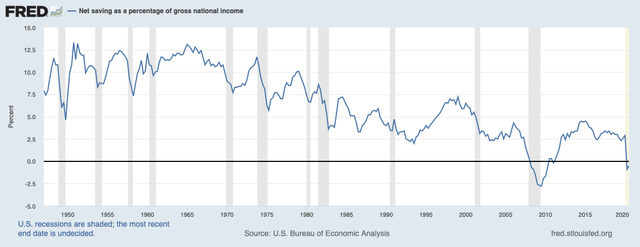

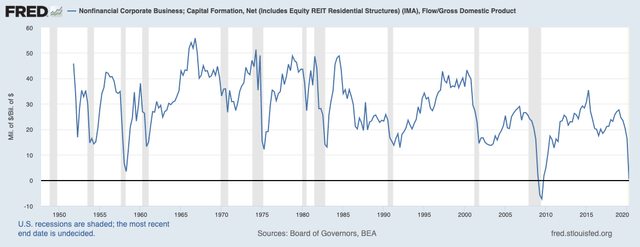

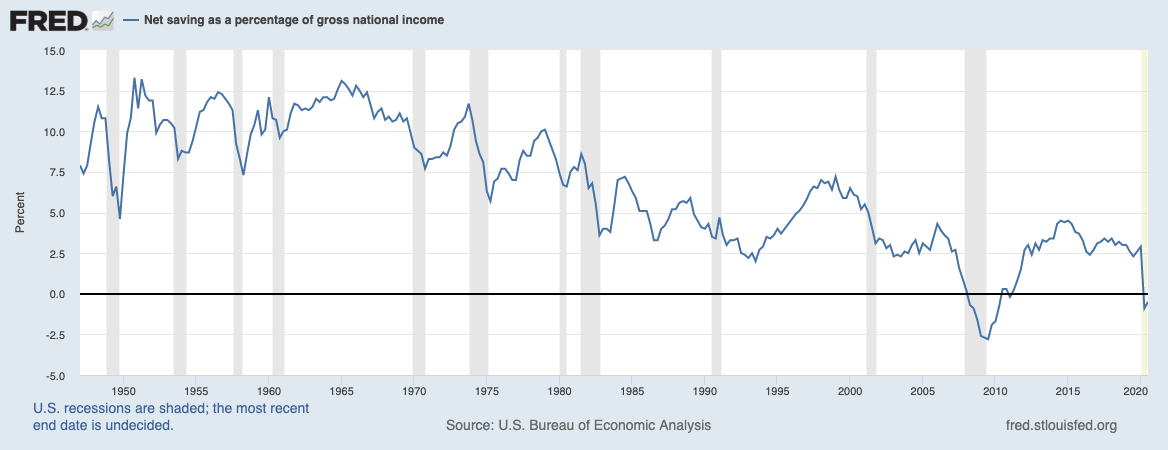

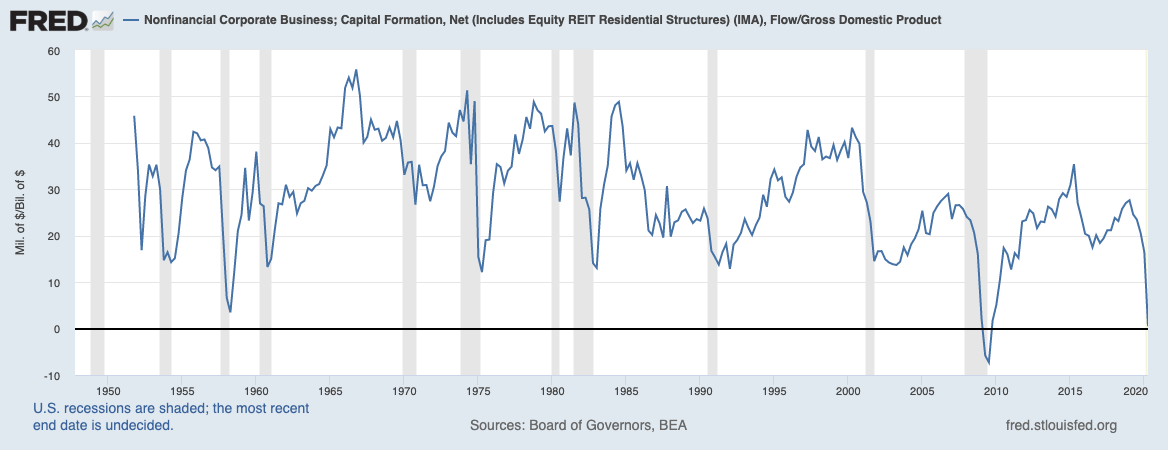

By necessity, private savings go to funding fiscal deficits first, because government debt is "risk free" (except for the risk of inflation). So when fiscal deficits rise faster than private savings, private investment—the fuel of economic growth—inevitably diminishes. Compare, for instance, US net national saving (private savings minus public deficits) and net capital formation (a proxy for private investment) to GDP:

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

2. Peak global population (and subsequent decline) is in sight.

Probably the most predictable of the social sciences is demography. And of all inquiries in demography, population growth is among the most predictable measurements. If you know how many babies are born, how many immigrants are coming in and going out, and the average lifespan, it's fairly easy to discern what population numbers are going to be into the future — at least as far out as a human lifespan.

Why does population growth matter? Because it has acted as a crucial component of economic growth over the last few centuries. For two reasons, one pertaining to consumption and the other pertaining to production.

More people in a certain country means more mouths to feed, more bodies to clothe and shelter, more demand for all kinds of goods and services (the consumption side). But more people also correlates with a larger labor force (the production side). More organic growth in demand via population growth (rather than debt) leads to more jobs.

The formula for GDP can be broadly thought of as:

Total labor force x labor productivity.

Flat labor force growth combined with rising labor productivity results in economic growth, as does a growing labor force combined with flat labor productivity. But if there is little or no growth in the labor force or in labor productivity, then neither will there be GDP growth.

To estimate future economic growth, then, it'll be useful to look at productivity and the labor force.

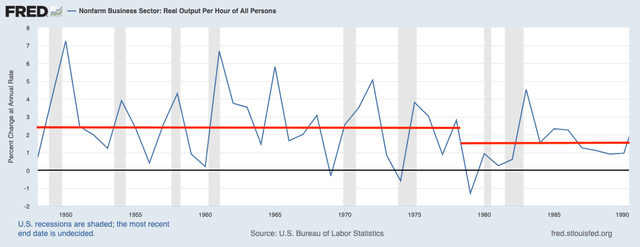

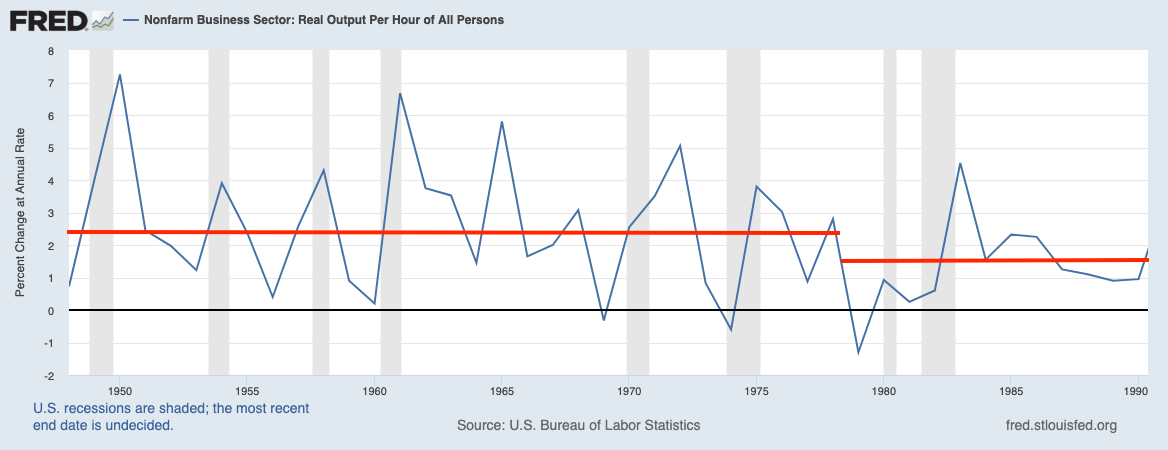

US labor productivity growth (year-over-year) averaged around 2.5% from the end of World War II to the mid-1970s, then took a step down to around 1.5% from the late 1970s through the 1980s.

This elevated labor productivity growth had multiple causes, including America's unique position as the world's industrial powerhouse after other developed nations had been obliterated in WWII. Another—not insignificant—factor, in my opinion, is the high private sector investment to GDP level enjoyed from 1950 through 2000.

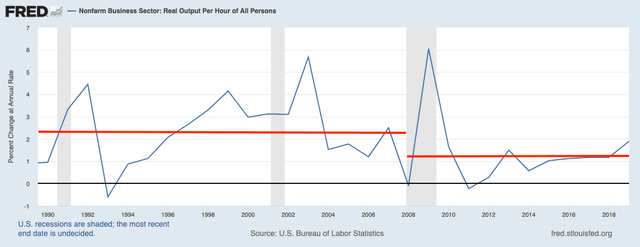

Then, from the 1990s through the mid-2000s, labor productivity growth averaged a little over 2% again, though it was on the decline even in the years before the Great Recession hit.

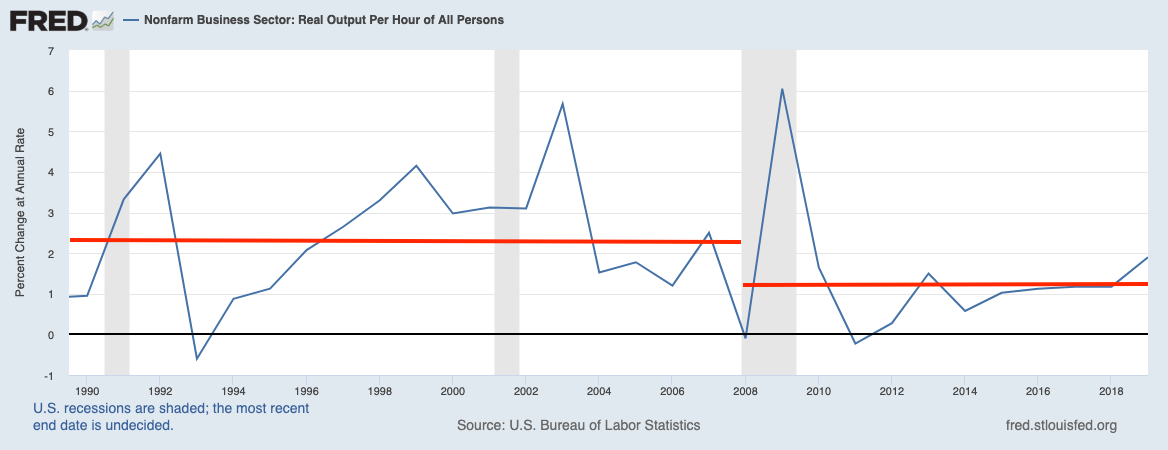

Notice, however, how weak productivity growth was in the post-Great Recession decade of the 2010s, averaging only slightly above 1%. If not for the spike in annual productivity growth in the wake of the recession, the average would be slightly under 1%.

As total private and public debt levels rise, we should expect to see labor productivity growth continue to drop over time.

How about the labor force? Well, as stated previously, growth in the labor force is largely dependent upon growth in the total population. This requires either births, net migration, or a combination of the two to significantly and sustainably outnumber deaths.

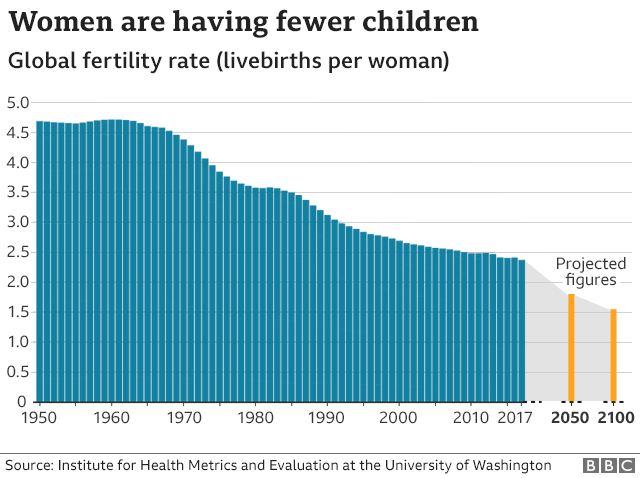

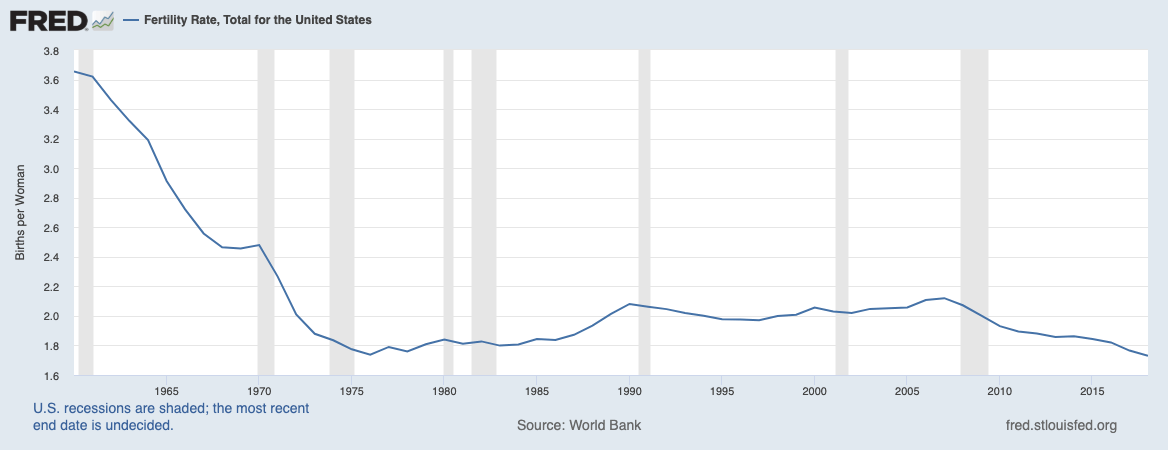

But even maintaining a stable population requires a fertility rate of 2.1 children per woman, assuming zero net migration and no changes to the mortality rate. Globally, childbirth per woman has been falling steadily (aside from a brief pause in the early 1980s) since the mid-1960s.

Researchers at the University of Washington recently projected that the global fertility rate would fall below 2.1 around 2030 and slump further to about 1.5 by 2100. Around 1.4 or 1.5 children per woman is where the researchers expect the long-term fertility rate to settle.

The primary drivers of the falling global fertility rate are education for women and access to contraceptives. Although, as I've argued elsewhere, consumer and education debt as well as stagnant real wage growth also play a significant part in the decline. In 1950, the global fertility rate was 4.7 children per woman. By 2017, that rate almost halved to 2.4.

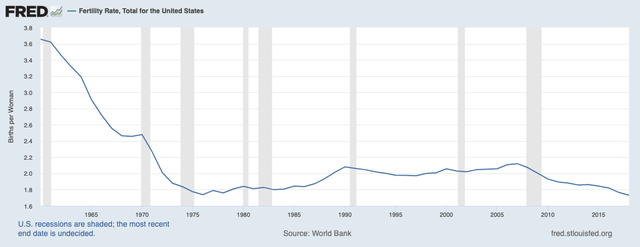

How about the fertility rate for the United States specifically? Despite a sharp drop in the birth rate from 1960 to 1975, US fertility has held steady and even risen slightly since the trough in 1976. At least, that was true up until the Great Recession, after which the birth rate began falling again.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers.

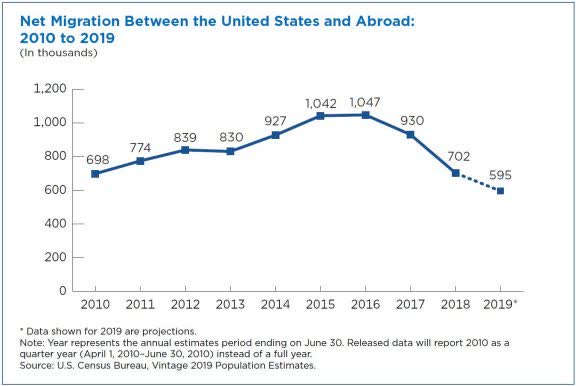

Luckily for the United States, net migration (immigrants coming in minus immigrants going out) has offset a birth rate under 2.1 children per woman and allowed the US population to continue growing. Not-so-luckily for the US, net migration has been falling off rather rapidly since 2016:

Hence we find that total US population growth slowed from 2014-2016's 0.7% to 0.6% in 2017 and 2018 and 0.5% in 2019. Last year's year-over-year population change marked the slowest growth in exactly one hundred years—since 1919.

If you think that's bad, look around the globe. Between now and 2100, the US population is expected to grow slightly or remain roughly flat. Many other nations are not so fortunate, according to the forecasts.

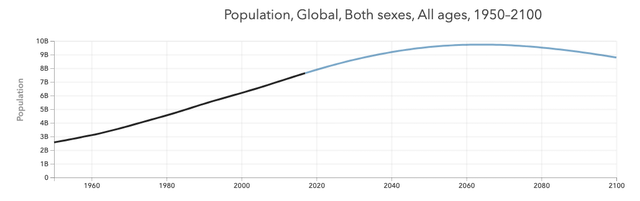

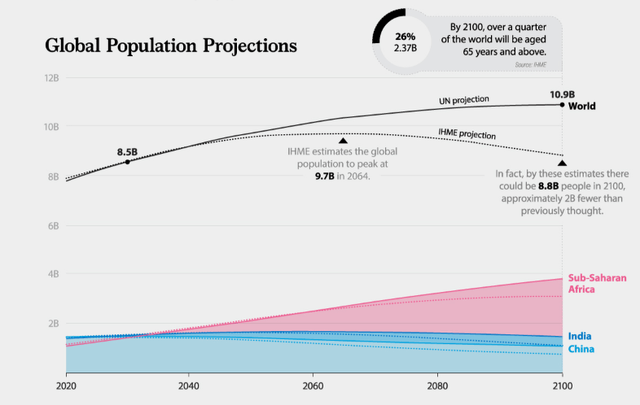

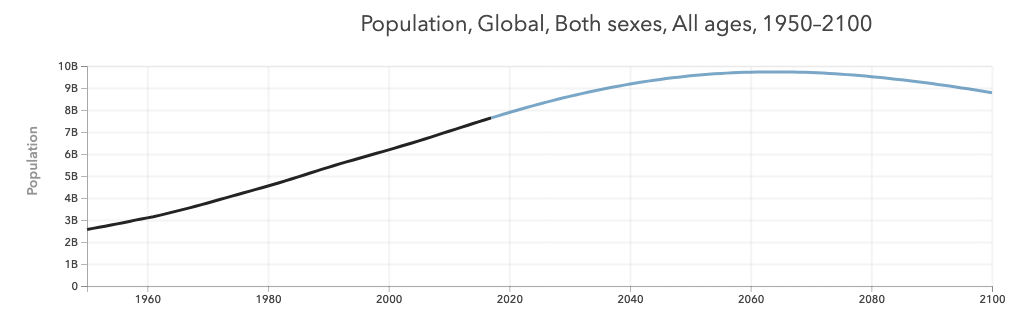

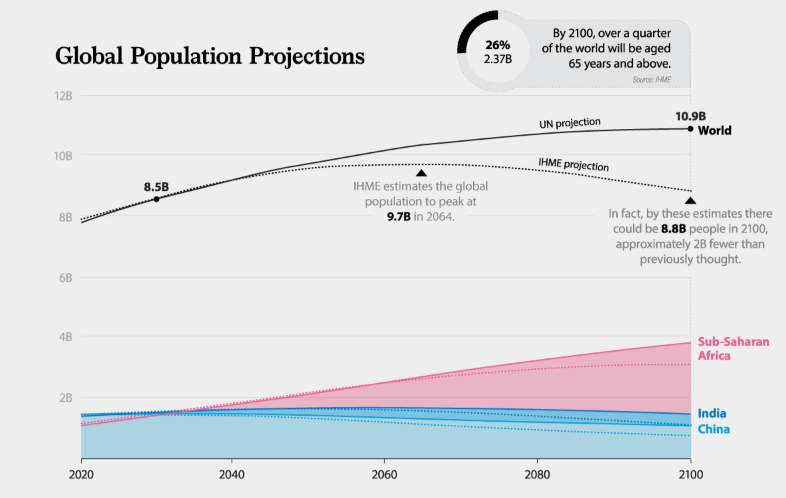

One recent expert population forecast, contrary to the last major forecast put out by the United Nations, projects the global population peaking well before the end of the current century and gradually declining thereafter.

In 2064, the global population is projected to peak and plateau for a few years at 9.73 billion people. Thereafter, it is expected to decline by nearly one billion people by 2100.

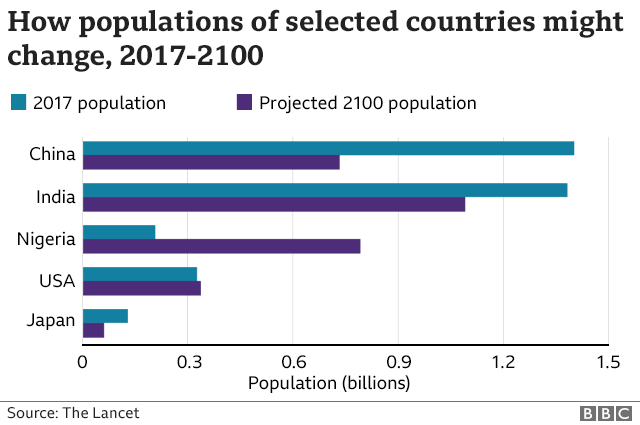

The situation is worse in many individual countries. The populations of Spain, Japan, and China are expected to halve between their 2017 populations and the year 2100. Meanwhile, astonishingly, the population of Nigeria is forecast to be higher than that of China by the end of the century, while the US population remains roughly unchanged.

Okay, so population growth is slowing and will continue to slow around the world until hitting roughly zero in the US and negative territory in many other parts of the world. Let's revisit the labor force.

Like slowing population growth, we also find a strong secular decline in labor force growth. Measuring total labor force growth by decade, we can see when the Baby Boomers flooded into the workforce in the 1960s, 1970s, and 1980s, with labor force growth falling off thereafter.

1950s: 11.5%

1960s: 18.4%

1970s: 29.6%

1980s: 17.2%

1990s: 12.6%

2000s: 9.2%

2010s: 7.5%

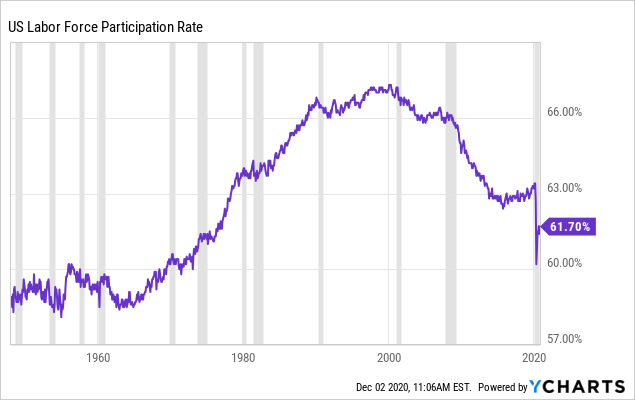

The falling labor force growth is not solely due to slower population growth, though the two are linked. Falling labor force participation among those of working age is also a factor. Interestingly, after 2000, at which time the critical mass of debt began causing drags on other growth metrics, the labor force participation (LFP) rate also began dropping. A severe slide occurred in the wake of the Great Recession, with very little rebound in the late 2010s.

It very well could be the case that the COVID-19 pandemic/recession will permanently reset the LFP rate lower.

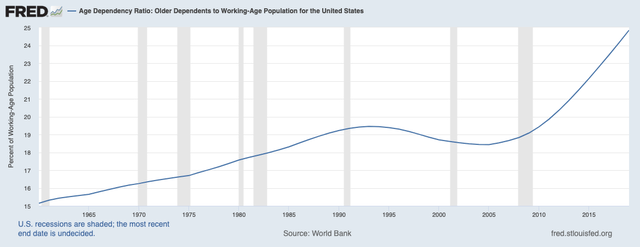

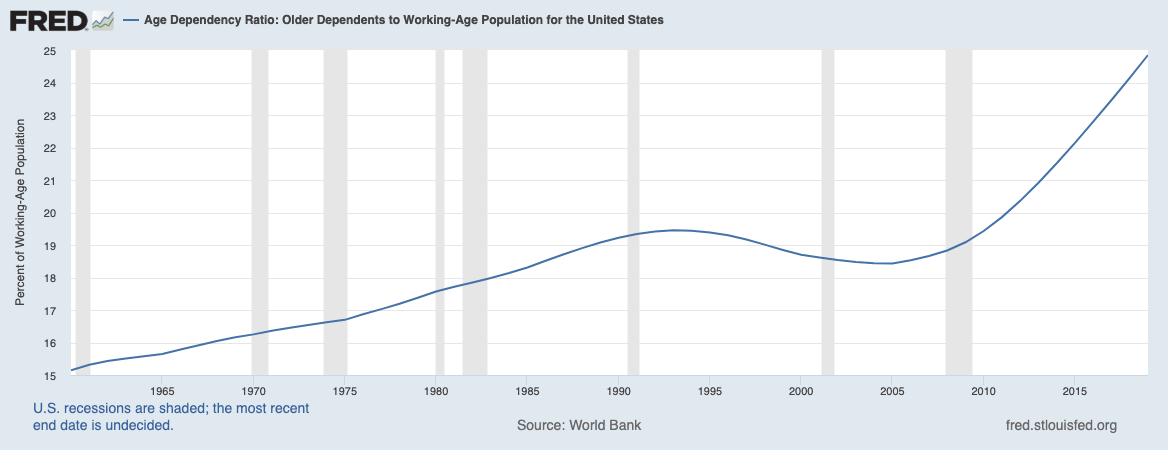

Notice above how LFP slightly edged upward from around 2003-2005. If we look at the age dependency ratio, which shows the number of retiree-aged Americans (65 and up) as a percentage of the working age population (15-64), we find that slightly edged downward during this same period of the mid-2000s, ending around 2005. Afterward, the ratio of retiree-aged Americans to the working-age population has shot up dramatically.

In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

This is what is sometimes referred to as the "silver tsunami."

In combination with a falling fertility rate, this trend of a rising dependency ratio is worrisome, as seniors require a lot more transfer payments than working-aged people, and transfer payments make up a majority of developed countries' government spending. This makes it highly unlikely that government spending will be cut, and thus deficit spending will likely remain as well.

So, we have an aging population and declining labor force growth, and we also have declining labor productivity growth.

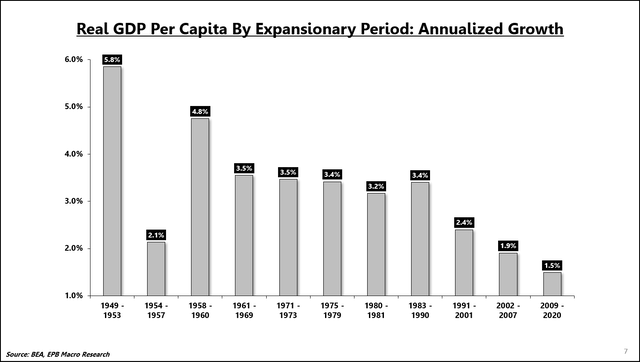

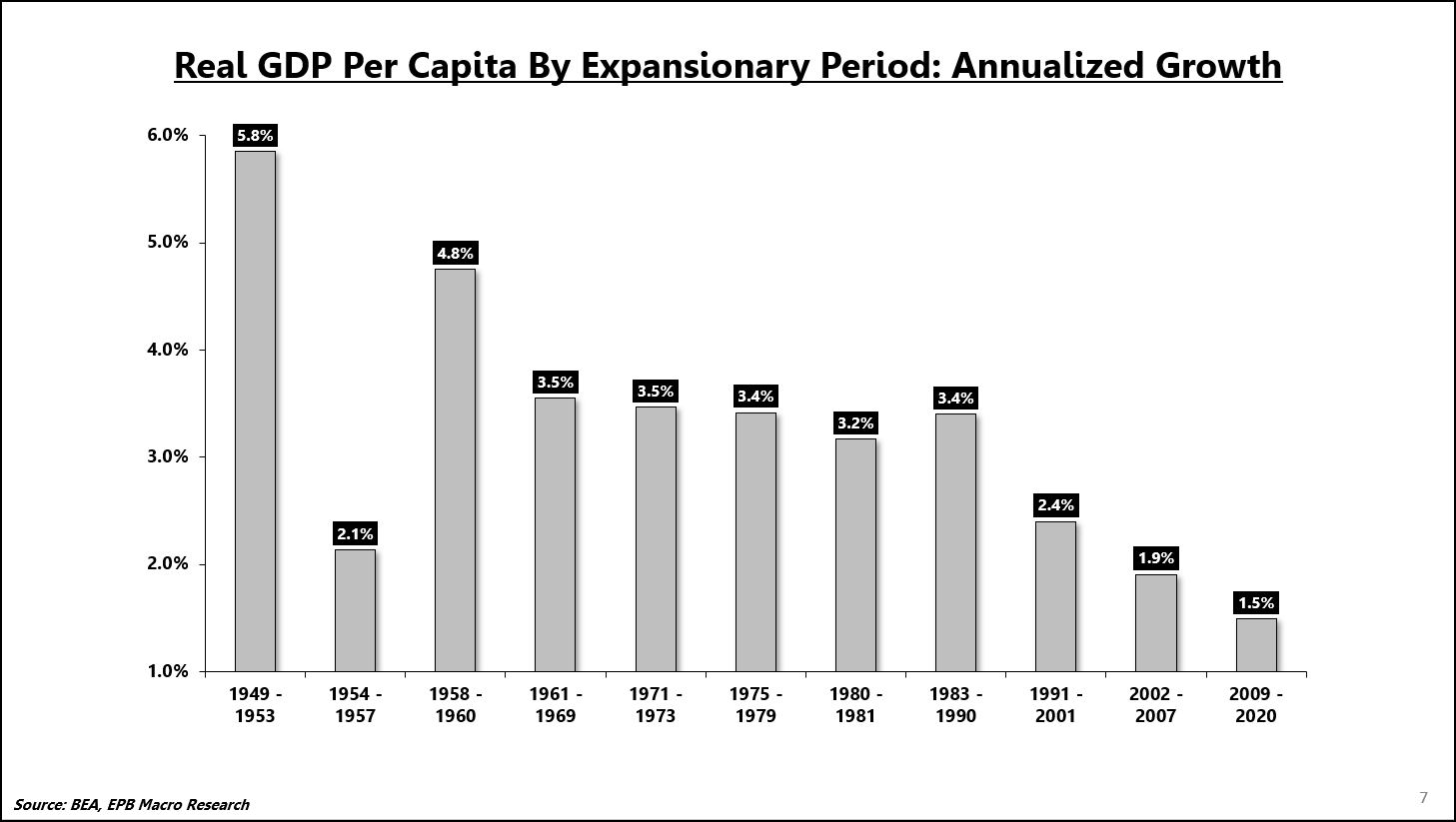

Unsurprisingly, then, we find that annual growth of real GDP per capita, a proxy for the national standard of living, has declined during every expansionary period since 1990.

It would not be surprising to see real GDP per capita rising at under 1% per year during the next economic expansion.

Conclusion

Never in recorded human history has the global population shrunk over a sustained period of time. Neither has there been any period of history in which the world has carried as much debt as it does today. The confluence of these factors is truly unprecedented. But, like the glacial advance of an ice age, it is happening at a slow enough pace to prevent raising as much alarm as is merited.

Predictions are very difficult to make in such unprecedented circumstances, but a few seem merited.

First, governments around the world will move heaven and earth to prevent deflation. Of course, fiscal policymakers won't call it "deflation" but instead will use more politically popular language like stimulating the economy or creating good jobs. Monetary policymakers, who more often come from the banking world, know that sustained deflation is a grave enemy. All else being equal, mild deflation has a lot of benefits. But in an economy that runs on continual debt-fueled consumption, the damage done to borrowers (who have to repay their debt in more valuable dollars) is highly destructive.

Second, the proxy metric for the standard of living, real GDP per capita, will continue to see duller and duller growth in the decades ahead, just like it has in Japan over the last few decades. It's simply a function of slowing labor force growth and slowing labor productivity growth. Less population growth, combined with generous transfer payment systems and other factors that make it feasible for some people to opt out of the labor force, translates into less labor force growth. And profligate deficit spending crowds out private investment, which will dampen labor productivity growth.

Third, at some point, economic pressures will force developed nations to switch from a posture of immigration restriction to one of desperation for immigrants, especially high-skilled ones. In fact, we are already at that point, but political pressures are holding back the economic pressures in many countries.

As a Millennial, I will probably live to see the peak of human population, although I will be part of the "silver tsunami" by then. If all of the above data and predictions are accurate, then my lifetime is likely to be an economically and geopolitically eventful one. Of course, even the next 10-20 years should also be interesting.

The more I think through the situation ahead, the more bullish I become on high-yielding but relatively safe assets, as these will be in high demand among the massive and growing older population that want to retire in comfort. My pessimism for the global economy translates into optimism for the relatively safe yields of well-chosen REITs, utilities, business development companies, and other dividend stocks.

At High Yield Landlord, these assets have been our exclusive focus and will remain so in the years to come.

Ice Ages, Old And New

The last ice age ended around 14,000 years ago, according to the geological consensus, during the Pleistocene Epoch. It lasted a long, long time. In fact, some remnants of the last ice age remain today. Glaciers in Greenland and Antarctica have been slowly receding since the Pleistocene era.

During an ice age, glacial ice sheets advance from the poles toward the equator, never covering the entire planet. Actually, the glaciers were constantly in flux, advancing and receding and advancing and receding, although that flux would barely be noticeable in a human lifetime.

During an ice age, the earth overall was much colder and drier. Variations in the weather sometimes caused the ice to advance faster than many species could adapt or move, and many went extinct because of it. Around three-fourths of all large animal species (mainly vertebrate mammals) completely died out during this period.

Saber-toothed tigers, mastodons, and woolly mammoths are examples. Much plant life also perished, even in areas that weren't covered in ice. Whole forests were consumed by the glacial advance. Entire ecosystems disappeared. The biological progression of life was put on pause, or even reversed, during this cold, dour period.

But scientists also believe that it was the Pleistocene ice age that formed humans into basically the creatures we are today. As migratory herds of animals moved toward the warmer parts of the earth around the equator, humans followed. Over many generations, these hunter-gatherer bands developed tools and complex clothing and learned to survive wherever they went. They were forced by a harsh environment to become smarter and more advanced.

You may already see where I'm going with this metaphor. For multiple reasons, I believe the global economy is now entering what I think of as an "economic ice age."

Just as the ice age of history caused a long pause or even contraction in the biological progression of life on earth, I think the "ice age" we are entering will cause a long pause or even contraction in humanity's economic progression. For a long time to come, our standards of living will rise at a crawling pace or perhaps even remain flat. Innovation will be incremental and concentrated in certain areas rather than the widespread leaps and bounds of advancement enjoyed over the 20th century.

There are several factors at play in the global economy today that bring me to this view, even while I remain optimistic about certain asset classes going forward. In this first installment, I want to discuss two of the biggest tectonic forces at play in the economic world today and finish with three predictions.

Just like the humans of the last ice age, we investors will need to become smarter and more adaptive in the years and decades to come.

Interest rates are sitting at zero, making credit cheaper. Cheaper credit spurs ballooning debt, even while investors around the world are desperate to find yield, thus keeping yields and interest rates low. But more debt, especially when it is taken out to fund consumption rather than productive investment, cripples the economy's ability to expand.

I've written about this on many occasions in the past. (See, for instance, "The Monetary Death Spiral.") There are basically three ways to pay for government spending: tax revenue, debt issuance, or money printing (which is inherently inflationary). All else being equal, fiscal deficits soak up domestic private savings, which reduces economic growth by crowding out private investment. But it can also be funded through increased trade deficits: Foreigners give us goods, we give them dollars, and they buy our government debt.

It's easy to see how this forms a self-reinforcing cycle: more debt leads to lower growth leads to more debt leads to lower growth. This leads to the inability of central banks to let rates rise, because in a highly indebted economy, even a small rise in rates causes debt service costs to soar.

As we can see in the chart below, federal government debt to GDP is now higher than at any time in our nation's history, including the peak of World War II.

Zooming in to the period from 1990 to today, we find that total credit market (public and private) debt has increased at roughly double the rate of GDP:

In my view, the persistent focus from policymakers on increasing consumption, even at the expense of a higher debt load, is short-sighted. It isn't that more government spending and stimulus can't produce temporary bursts of growth or fill the chasm in consumption caused by the pandemic. It can.

But there are two problems. First, such spending necessarily must come from either taxes (private sector income), debt (private savings), or an increased trade deficit (foreign investors that cannot be relied on permanently). Money printing is not legally an option for the government at this point. Second, it misunderstands how economies grow over time.

By necessity, private savings go to funding fiscal deficits first, because government debt is "risk free" (except for the risk of inflation). So when fiscal deficits rise faster than private savings, private investment—the fuel of economic growth—inevitably diminishes. Compare, for instance, US net national saving (private savings minus public deficits) and net capital formation (a proxy for private investment) to GDP:

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

2. Peak global population (and subsequent decline) is in sight.

Probably the most predictable of the social sciences is demography. And of all inquiries in demography, population growth is among the most predictable measurements. If you know how many babies are born, how many immigrants are coming in and going out, and the average lifespan, it's fairly easy to discern what population numbers are going to be into the future — at least as far out as a human lifespan.

Why does population growth matter? Because it has acted as a crucial component of economic growth over the last few centuries. For two reasons, one pertaining to consumption and the other pertaining to production.

More people in a certain country means more mouths to feed, more bodies to clothe and shelter, more demand for all kinds of goods and services (the consumption side). But more people also correlates with a larger labor force (the production side). More organic growth in demand via population growth (rather than debt) leads to more jobs.

The formula for GDP can be broadly thought of as:

Total labor force x labor productivity.

Flat labor force growth combined with rising labor productivity results in economic growth, as does a growing labor force combined with flat labor productivity. But if there is little or no growth in the labor force or in labor productivity, then neither will there be GDP growth.

To estimate future economic growth, then, it'll be useful to look at productivity and the labor force.

US labor productivity growth (year-over-year) averaged around 2.5% from the end of World War II to the mid-1970s, then took a step down to around 1.5% from the late 1970s through the 1980s.

This elevated labor productivity growth had multiple causes, including America's unique position as the world's industrial powerhouse after other developed nations had been obliterated in WWII. Another—not insignificant—factor, in my opinion, is the high private sector investment to GDP level enjoyed from 1950 through 2000.

Then, from the 1990s through the mid-2000s, labor productivity growth averaged a little over 2% again, though it was on the decline even in the years before the Great Recession hit.

Notice, however, how weak productivity growth was in the post-Great Recession decade of the 2010s, averaging only slightly above 1%. If not for the spike in annual productivity growth in the wake of the recession, the average would be slightly under 1%.

As total private and public debt levels rise, we should expect to see labor productivity growth continue to drop over time.

How about the labor force? Well, as stated previously, growth in the labor force is largely dependent upon growth in the total population. This requires either births, net migration, or a combination of the two to significantly and sustainably outnumber deaths.

But even maintaining a stable population requires a fertility rate of 2.1 children per woman, assuming zero net migration and no changes to the mortality rate. Globally, childbirth per woman has been falling steadily (aside from a brief pause in the early 1980s) since the mid-1960s.

Researchers at the University of Washington recently projected that the global fertility rate would fall below 2.1 around 2030 and slump further to about 1.5 by 2100. Around 1.4 or 1.5 children per woman is where the researchers expect the long-term fertility rate to settle.

The primary drivers of the falling global fertility rate are education for women and access to contraceptives. Although, as I've argued elsewhere, consumer and education debt as well as stagnant real wage growth also play a significant part in the decline. In 1950, the global fertility rate was 4.7 children per woman. By 2017, that rate almost halved to 2.4.

How about the fertility rate for the United States specifically? Despite a sharp drop in the birth rate from 1960 to 1975, US fertility has held steady and even risen slightly since the trough in 1976. At least, that was true up until the Great Recession, after which the birth rate began falling again.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers.

Luckily for the United States, net migration (immigrants coming in minus immigrants going out) has offset a birth rate under 2.1 children per woman and allowed the US population to continue growing. Not-so-luckily for the US, net migration has been falling off rather rapidly since 2016:

Hence we find that total US population growth slowed from 2014-2016's 0.7% to 0.6% in 2017 and 2018 and 0.5% in 2019. Last year's year-over-year population change marked the slowest growth in exactly one hundred years—since 1919.

If you think that's bad, look around the globe. Between now and 2100, the US population is expected to grow slightly or remain roughly flat. Many other nations are not so fortunate, according to the forecasts.

One recent expert population forecast, contrary to the last major forecast put out by the United Nations, projects the global population peaking well before the end of the current century and gradually declining thereafter.

In 2064, the global population is projected to peak and plateau for a few years at 9.73 billion people. Thereafter, it is expected to decline by nearly one billion people by 2100.

The situation is worse in many individual countries. The populations of Spain, Japan, and China are expected to halve between their 2017 populations and the year 2100. Meanwhile, astonishingly, the population of Nigeria is forecast to be higher than that of China by the end of the century, while the US population remains roughly unchanged.

Okay, so population growth is slowing and will continue to slow around the world until hitting roughly zero in the US and negative territory in many other parts of the world. Let's revisit the labor force.

Like slowing population growth, we also find a strong secular decline in labor force growth. Measuring total labor force growth by decade, we can see when the Baby Boomers flooded into the workforce in the 1960s, 1970s, and 1980s, with labor force growth falling off thereafter.

1950s: 11.5%

1960s: 18.4%

1970s: 29.6%

1980s: 17.2%

1990s: 12.6%

2000s: 9.2%

2010s: 7.5%

The falling labor force growth is not solely due to slower population growth, though the two are linked. Falling labor force participation among those of working age is also a factor. Interestingly, after 2000, at which time the critical mass of debt began causing drags on other growth metrics, the labor force participation (LFP) rate also began dropping. A severe slide occurred in the wake of the Great Recession, with very little rebound in the late 2010s.

It very well could be the case that the COVID-19 pandemic/recession will permanently reset the LFP rate lower.

Notice above how LFP slightly edged upward from around 2003-2005. If we look at the age dependency ratio, which shows the number of retiree-aged Americans (65 and up) as a percentage of the working age population (15-64), we find that slightly edged downward during this same period of the mid-2000s, ending around 2005. Afterward, the ratio of retiree-aged Americans to the working-age population has shot up dramatically.

In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

This is what is sometimes referred to as the "silver tsunami."

In combination with a falling fertility rate, this trend of a rising dependency ratio is worrisome, as seniors require a lot more transfer payments than working-aged people, and transfer payments make up a majority of developed countries' government spending. This makes it highly unlikely that government spending will be cut, and thus deficit spending will likely remain as well.

So, we have an aging population and declining labor force growth, and we also have declining labor productivity growth.

Unsurprisingly, then, we find that annual growth of real GDP per capita, a proxy for the national standard of living, has declined during every expansionary period since 1990.

Image Source (Modified by Author)

Image Source (Modified by Author) Image Source (Modified by Author)

Image Source (Modified by Author) Data by YCharts

Data by YCharts

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

Notice how both metrics peaked around the same time in the mid-1960s while also passing together into negative territory for the first time in the post-war period during the Great Recession. Around the year 2000, total debt reached a critical mass in the United States such that the peaks and troughs of private investment took a dramatic step down. Now, predictably, with net savings in negative territory and an ongoing pandemic, private investment has once again plummeted.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers.

Source: Institute For Health Metrics And Evaluation - Population Forecasting

Source: Institute For Health Metrics And Evaluation - Population Forecasting Source: Visual Capitalist

Source: Visual Capitalist

Data by YCharts

Data by YCharts In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers.

In 2018 (and 2019), the US had a fertility rate of 1.73 live births per woman, slightly lower than the lowest point hit in the 1970s. While births in 2020 are likely to come in somewhere in the same range as the previous few years, there is strong evidence that births will fall by about half a million in 2021 due to COVID-19, say Brookings Institution researchers. Source: Institute For Health Metrics And Evaluation - Population Forecasting

Source: Institute For Health Metrics And Evaluation - Population Forecasting Source: Visual Capitalist

Source: Visual Capitalist In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

In 1960, the retiree-aged population made up about 15% of the working-age population. Today, they make up about 25% of the working-age population, and that percentage is set to continue rising over the coming decades.

No comments:

Post a Comment