Is Palantir The Next Facebook Or The Next Myspace?

Palantir has continued to perform incredibly well, but that doesn't change the fact that it's priced for massive growth.

Facebook managed to drive strong shareholder financial rewards as it grew, while Myspace made bad moves chasing growth.

We see Palantir as the next Facebook, due its strong financial improvements and focus, but the company does have risks worth looking at.

I do much more than just articles at The Energy Forum: Members get access to model portfolios, regular updates, a chat room, and more. Get started today »

Palantir Technologies (PLTR) has had a great November, growing its market capitalization to more than $50 billion. In the space of tech IPOs, this isn't particularly unique. However, the question becomes, how much runway is left. In the social media world, there's two classic companies.

Myspace, the largest worldwide social network from 2005-2009, never truly figured out how to monetize its user base, putting too many ads, becoming uncompetitive, and losing its user base. Facebook (FB) managed to efficiently and thoroughly monetize its user base, and is now a near-$1 trillion company with an incredible FCF profile. Since its post IPO lows, the company has returned nearly 15x to shareholders.

As we'll see throughout this article, we view Palantir as the next Facebook due to its unique characteristics.

![]()

(Palantir - Wccftech)

Company Overview

Palantir is a large American public software company that specifies in Big Data analytics. Big Data analytics is a complicated and involved field, which requires a massive number of hardworking engineers and significant years of experience to be able to understand how to not only best provide those analytics, but turn them into useful consumable data.

That's something that most companies don't have the know-how, financial ability, or willingness to do. However, it's something that nearly every business can benefit from, and something that's immensely popular. Palantir is a unique player here, often the only consumer in its space, and it has the potential to drive significant rewards.

Company's Contracts and Businesses

Palantir's unique businesses means that the company has achieved a number of unique businesses.

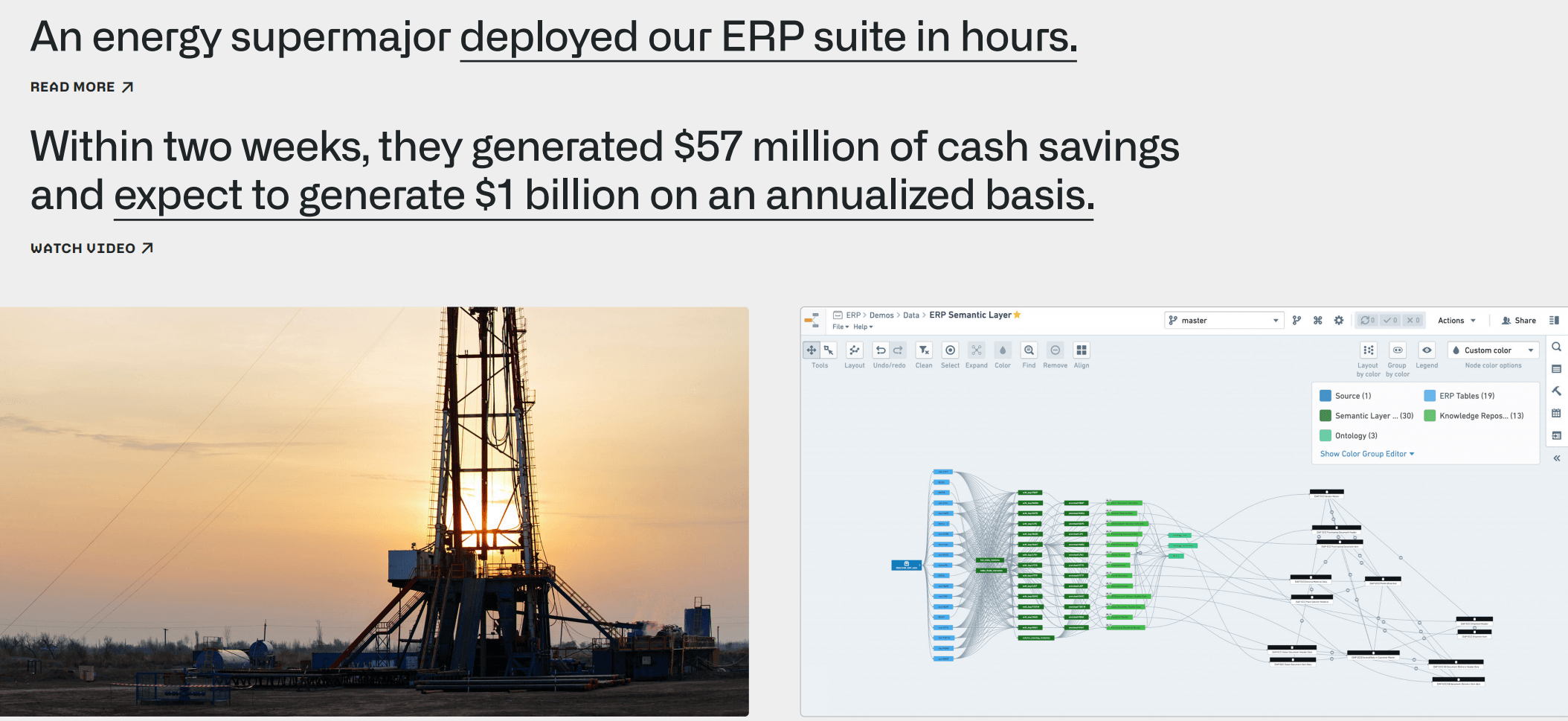

(Palantir Energy Supermajor - Palantir Investor Presentation)

Palantir, through the worst energy collapse in 2020 due to COVID-19, saw an energy supermajor deploy its ERP suite. That deployment, within 2 weeks, allowed $57 million in cash savings and is expected to be able to drive $1 billion in savings on an annualized basis. The value of Palantir's assets are clear here, and it highlights the value of the company's assets.

The U.S. Justice Department versus Purdue Pharma, the World Food Programme, and U.S. Special Forces. The company, as we'll see through the financial section, is continuously getting new contracts, helping its customers, and doing incredibly well with its customers. Another recent contract was a $91 million 2-year deal with the U.S. Army Research Laboratory.

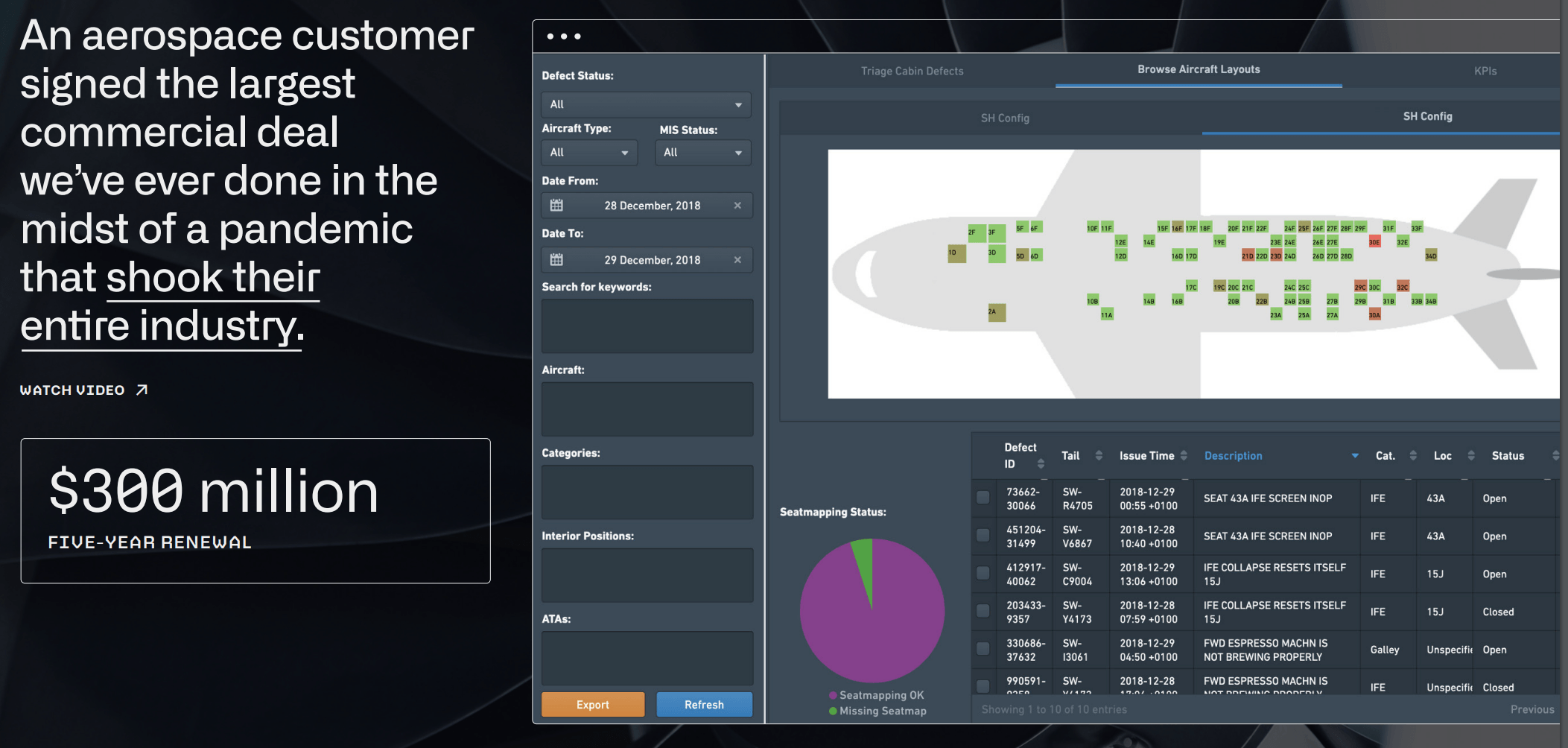

(Palantir New Aerospace Company - Palantir Investor Presentation)

As COVID-19 has shaken up industries around the world, companies have been forced to adapt and look for savings, and Palantir has been at the forefront of that. The aerospace agency is one of those that has suffered the most due to COVID-19, and it's simultaneously one of the industries with the most room for Big Data improvements.

Palantir's $300 million 5-year renewal deal here is not only the start, but it highlights the financial potential.

3Q Financials

On the back of this, it's worth discussing Palantir's recent 3Q financial performance, which has boosted the share price significantly.

(Palantir 3Q 2020 Financials - Palantir Investor Presentation)

Palantir has seen its revenue increase 52% YoY to almost $1.2 billion annualized. That means that the company is trading at an incredibly high multiple of roughly 40x price-to-sales. The company's operating income has switched from a $92 million loss in 3Q 2019 to $73 million in 3Q 2020, representing even more significant YoY growth.

However, the key takeaway here isn't that Palantir's growing, it's that it needs massive growth. The company eventually needs to be several dozen times its current size, in order to justify its valuation.

Overall Financial Growth

Fortunately, Palantir's overall financial growth is significant, and the company has significant potential to drive shareholder returns.

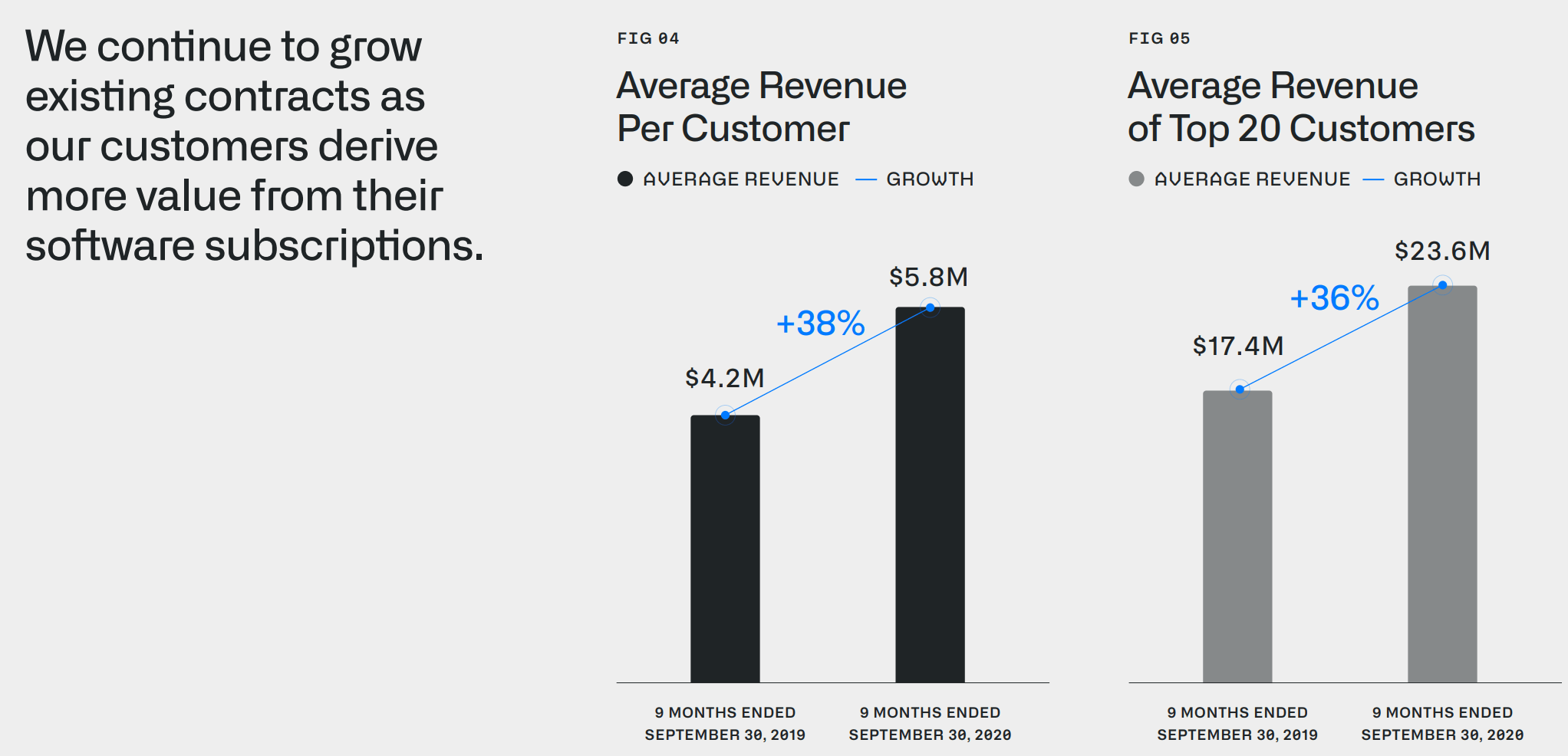

(Palantir Growth - Palantir Investor Presentation)

For those who've never participated in the business to business sales industry, it's a tough and slow-moving business regardless of your company's size. Fortunately, Palantir's worked to handle that by growing its average revenue per customer and its average revenue of top customers, in addition to getting new customers.

The company's average revenue per customer has gone up 38% YoY, while the average revenue of its top 20 customers has gone up 36% YoY. Simultaneously, Palantir's top 20 customers have gone down from 68% of its revenue to 61% of revenues. As customers continue to utilize the software and expand it, the company has potential.

(Palantir Three Phase Guidance - Palantir Investor Presentation)

Palantir has continued to expand in the acquire phase, expand phase, and scale phase. The company has seen new customers provide significantly more revenue at less expense. In the expand phase and the scale phase, revenue is increasingly dramatically. The company's expand phase revenue for 2020 is almost at its 2019 scale phase revenue.

This comes with significantly more margins on these established businesses. The revenue growth (44% YoY) and operating margin growth (12% YoY) combined are enormous for Palantir. If the company can continue achieving this growth, it can rapidly justify its current valuation. Continued growth here is what investors should pay close attention to.

However, given the abilities of Palantir's software, we feel it's a likely-case scenario.

Risk

Palantir's risk is two-fold, and it's worth keeping close attention to both of these given the company's current valuation.

The first is that the company's growth might not continue. It has performed so far; however, tech is always a difficult business, and a business-to-business sales industry is slow and tough. However, the company's multiple requires growth, and Myspace, in chasing growth, made some bad moves in the rush. The same could befall Palantir.

The company's second risk is that it is unpopular due to some of the government groups it works with. While we believe that Palantir is a net benefit, it could face increased regulation or investigation into its businesses that come at a significant cost. That could significantly hurt the company's ability to drive shareholder rewards.

Conclusion

Palantir has continued to outperform, both from a share price perspective and from a business perspective. The company has a valuable portfolio of data technology assets, and in an as uncertain time as COVID-19, it has the potential to drive strong financial rewards for customers, although business-to-business sales are slow.

We see the company as the next Facebook, due to its improving financial capacity and ability to drive shareholder rewards here. However, we recommend keeping a close eye on whether or not that pans out. Palantir is worth a cautious investment at this time, as investors continue to pay attention to the growth story.

Create a High Yield Energy Portfolio - 2 Week Free Trial!

The Energy Forum can help you generate high-yield income from a portfolio of quality energy companies. Worldwide energy demand is growing and you can be a part of this exciting trend.

No comments:

Post a Comment