Only when it is exposed over time as false does the conformity break, and typically only if there are negative political consequences for Democrats. The saving grace is that sometimes reality is impossible to ignore, and 2021 was the year this happened on some of the biggest events of our time. It’s worth recounting a few examples to see how the dominant consensus was wrong about so much for so long.

• The Wuhan Virology Lab origin theory of Covid-19. In the early days of the pandemic, even raising this as a possibility was taboo. Sen. Cotton was vilified for doing so. The Lancet, a supposedly open-minded scientific journal, published a letter in February 2020 “to strongly condemn conspiracy theories suggesting that COVID-19 does not have a natural origin.”

This year we learned that the Lancet letter was part of a coordinated effort to quash the lab theory. We learned about the conflicts of interest of Anthony Fauci and others who provided funding for the Wuhan lab. Eventually even the press noticed that China had blocked an honest inquiry, and that no evidence for a natural origin has emerged.

• Lockdowns stop Covid-19. There was no fiercer consensus in the early days of the virus than the belief that locking down the economy to stop the virus was an unadulterated social good. We felt the consensus wrath when we raised doubts, in an editorial on March 20, 2020, about the harm that lockdowns would do to the economy and public health.

Two years later we now know that lockdowns at most delay the virus spread. The damage in lost education for children, lost livelihoods for workers and employers, and damage to mental health is obvious for all to see. Even Randi Weingarten, the teachers union chief who did so much to keep schools closed, now claims she wanted to keep them open all along.

• The supply side of the economy doesn’t matter. The Keynesian consensus, which dominates the U.S. and European media, has long held that the demand for goods and services drives the economy. The ability or incentive to supply those goods is largely ignored or dismissed. Spurring demand was the theory behind the trillions of dollars in spending by Congress and easy money from the Federal Reserve.

All that money did spur demand. But the Keynesians ignored the disincentives to increase supply from paying people not to work and restricting work with lockdowns and mandates. The result was the surging inflation that caught nearly all of them by surprise. Their demand-side models never saw it coming.

• The Steele dossier and Russia collusion narrative. In 2019 the Mueller report exposed the lack of evidence for the claims that Donald Trump and the Kremlin were in cahoots. This year the indictments by special counsel John Durham have revealed how Democrats and the press worked together to promote the dossier that was based on disinformation.

Yet for four years nearly everyone in the dominant media bought the collusion narrative. One or two of the gullible have apologized, but most want everyone to forget what they wrote or said at the time.

• Vilifying police won’t affect crime. The fast-congealing consensus after George Floyd’s murder was that most police were racist, as was most of American society, and violent protests against this were justified—even admirable. Woe to anyone who pointed out that the victims of these riots and crime were mostly poor and minority communities.

Police funding was cut and bail laws eased in many cities. Eighteen months later we see the result in rising crime rates and a soaring murder count. A political backlash now has even many Democrats claiming they really do want more funding for police.

In a recent Washington Post op-ed, three retired generals, Paul Eaton, Antonio Taguba, and Steven Anderson, warn of a supposedly impending coup should Donald Trump be elected in 2024.

The column seemed strangely timed to coincide with a storm of recent Democratic talking points that a re-elected Trump, or even a Republican sweep of the 2022 midterms, would spell a virtual end of democracy.

Ironies abound.

From Election Day in 2020 to Inauguration Day 2021, we were told by the Left that democracy was resilient and rightly rid the nation of Trump.

The hard Left, for one of the rare times in U.S. history, was now in complete control of both houses of Congress and the presidency.

Spiking inflation, supply-chain shortages, near-record gas prices, open borders, the flight from Afghanistan, multi-trillion-dollar deficits, and polarizing racial rhetoric all followed.

In response to these events, Joe Biden’s popularity utterly collapsed. His own cognitive challenges multiplied the unpopularity of his failed policies.

In reaction, the Left again pivoted. It suddenly announced that should it lose congressional power in 2022 or the presidency in 2024, democracy was all but doomed.

Apparently, what changed Democrats’ views was that democracy was working all too well in expressing widespread public disgust . . . with the Left.

Even more ironies followed.

The three retired generals shrilly write of the dangers of insurrection and coups. Yet the FBI found no such insurrection or conspiracy in the buffoonish riot on January 6.

The more they talk about a coup, the more likely one becomes. It’s destructive and deeply irresponsible, but then our political class is destructive and deeply irresponsible.

The long-term Treasury yields (or 10-year yield) remain stubbornly low, signaling a recession or deflation is coming soon.

Don't misinterpret Treasury yield signals. We are currently seeing dynamics that the market has not witnessed for over 70 years.

How did the stock markets do historically in periods of high inflation and low interest rates, similar to the one we are seeing today?

The Fed already fooled you about inflation this year. Don't be fooled by Powell's hawkish talk.

The Fed to remain dovish, inflation running high. How you can profit in the current environment?

Looking for a portfolio of ideas like this one? Members of High Dividend Opportunities get exclusive access to our model portfolio. Learn More »

bunhill/E+ via Getty Images

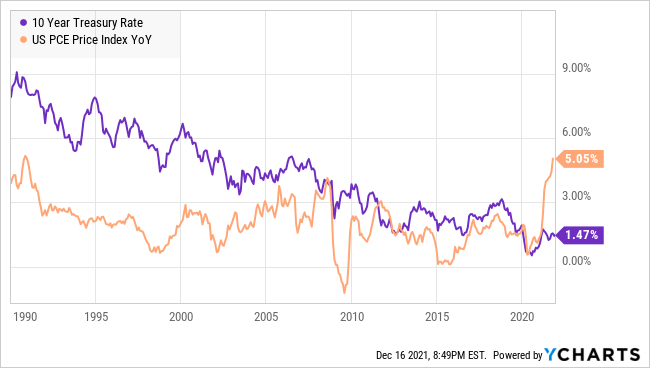

We have consistently been taught that we should always listen to what the Treasury yields are telling us. When inflation is running as high as it is today, you should expect one of two things from the Treasury yields:

Long-term treasury yields (or the 10-year yield) go up along with the inflation rate, which would suggest that the bond markets are pricing in a healthy economy, or

Long-term treasury yields (or the 10-year yield) remain the same or even go down, which would suggest that that the bond markets are pricing-in an economic recession along with a collapse of inflation.

With the 10-year yield remaining stubbornly low at 1.5%, many investors believe that they are pointing to a recession (or deflation) next year, whereby we could see a big market crash.

However today, we are seeing a very interesting phenomenon, unseen in modern times. Inflation (as measured by U.S. Personal Consumption Expenditures) is running well above the 10-year Treasury yields, resulting in significant negative "real yields"! Take a look at this chart since the year 1990 (or for the past 31 years).

Well, inflation is so high and persistent that even Jay Powell stopped using the word "transient", yet the 10-year Treasury yield is around 1.5%. This is confusing many investors who are asking themselves:

Are we heading into a deflationary environment?

Are we heading into a recession?

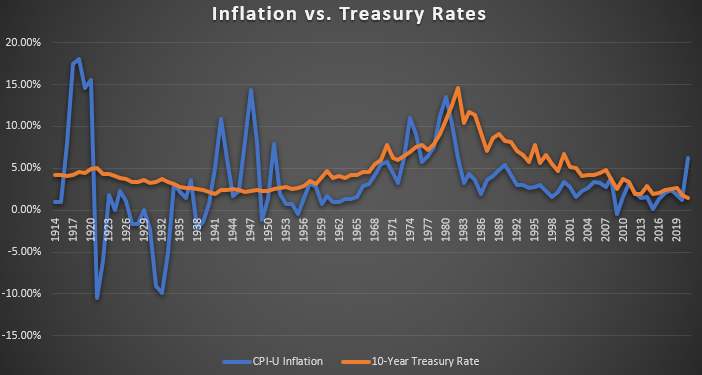

This is a very interesting phenomenon, that we have only seen 3 times in the past 120 years in the United States:

During the Civil War

During and after World War I

During and after World War II

The fourth time is happening right now!

Treasury yields always tell the right story, but it is people that misinterpret them.

A Dig Through History

It is very easy for us to fall into the trap of assuming things that have been true for 20+ years have been true "forever". This is called "recency bias", where our perspective of the world is more strongly influenced by things that happened recently than by things that happened long in the past.

When we think of high inflation, most of us jump right to the 1970s when higher inflation led to higher treasury yields, and treasuries almost always had a higher yield than inflation.

It's a period that many of us lived through or at least our parents lived through it. So it is a period that is fairly accessible. But has it always been the case?

No, it has not - if we dig into history:

Since the mid-1950s, we have seen a few cases when inflation has been higher than the 10-year Treasury rate, but the difference was resolved fairly quickly.

If we go further back in history, we have seen cases of inflation spiking up significantly, and the 10-year Treasury remaining low for a long period of time. The "real yields" were deeply negative as they are today. The two most obvious cases relate to World War I and World War II.

So what is the common denominator in WWI, WWII, and Today?

In all cases, for obvious reasons, debt spiked to unusual levels.

The Treasury markets are pricing-in continued loose monetary policy. The Government will let inflation take its course to "deflate" the national debt", rather than curb inflation as they have been telling us.

So it is no wonder that Treasury yields refuse to go higher than they are today! In fact, what treasuries are telling us is exactly what I have been saying over the past several months:

The Fed cannot and will not hike rates anytime soon. And if they do, it will be an immaterial rate hike that will have an insignificant impact on inflation.

The government will continue to ensure there is a high amount of liquidity in the financial system. The Bubble of Liquidity will remain large.

How Did the Markets Fare During Similar Periods: WWI and WWII

For us investors, it is important to not only be aware of what is happening in today's macro-economic situation but to also understand what the likely outcome will be for equities. In this case, we have to go back to the periods of WWI and WWII and see how equities fared during times of very high inflation and very low Treasury yields:

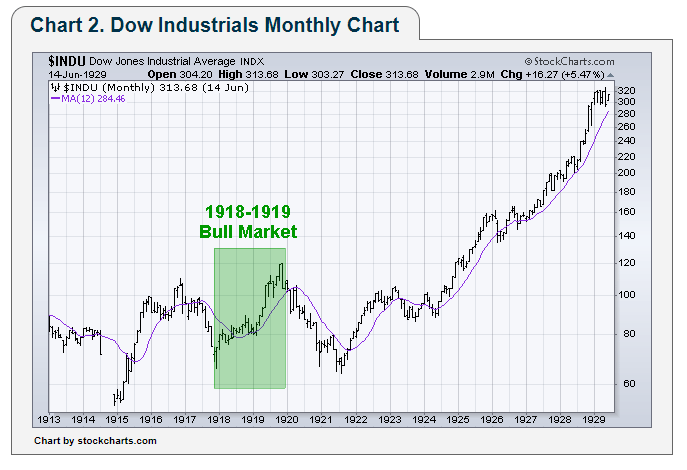

Case #1: WW I (Bull Market of 1918-1919)

Inflation started picking up significantly in 1917 when the U.S. formally got involved in WWI. Inflation surged up to 18% while the 10-year Treasury rate remained at 4.5%. Inflation remained high through 1919.

Despite an initial selloff in late 1917, we saw a great Bull Market that ran through 1918 and 1919 and the Dow Jones Industrial Average hit all-time highs. The Bull Market ran up 80% over the course of two years.

The party came to an abrupt end in 1920 when inflation suddenly became deflation. A few of the most relevant factors impacting the recession in 1920 were:

The return of troops from WW1: 1920 was characterized by high unemployment rates as troops coming home from war struggled to find work.

Resurgence in the Spanish Flu: The Spanish Flu was particularly brutal the 1919-1920 season, with the death rate approximately doubling.

The Gold Standard: In 1920, the dollar was still linked to gold. Deflation expectations were high, as people anticipated a wave of redemptions to reduce the monetary supply.

Rising Interest Rates: The Fed hiked rates in an effort to fight inflation from December 1919 through June 1920, from 4.75% to 7%.

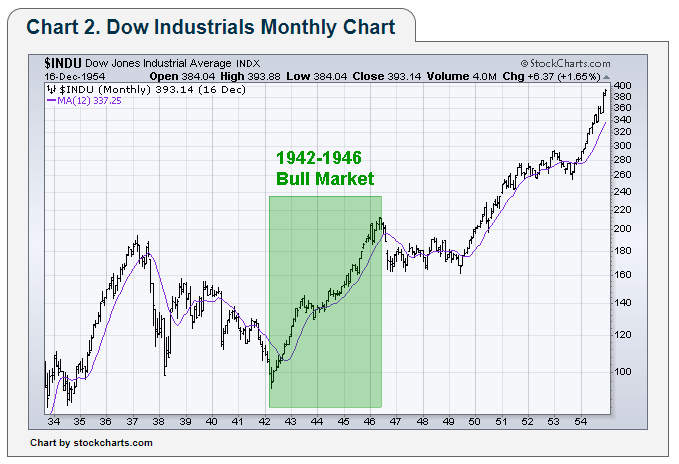

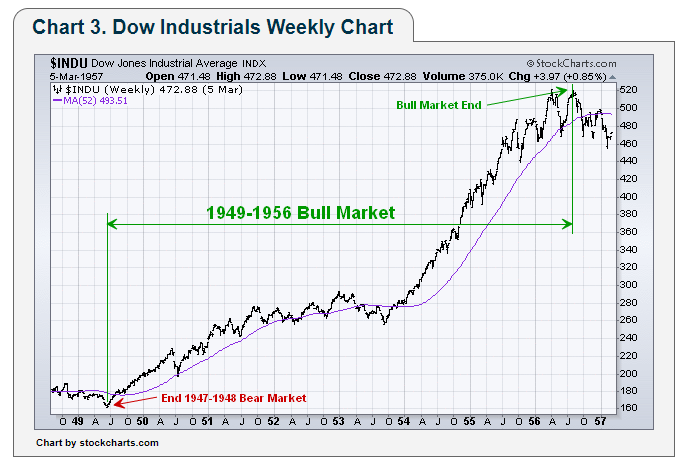

Case #2: WW2 (Bull Market 1942-1956)

From 1942-1956, we can see several periods where inflation significantly exceeded the 10-year Treasury rate. Over this 14-year period, inflation averaged over 4%, while the 10-year Treasury rate averaged 2.5%. Meanwhile, the DJIA averaged +11% per year. I believe this is the most comparable period to our situation today.

The DJIA gained 120% from 1942-1946, even as inflation outpaced the 10-year Treasury rate for three of those years.

The "bear" market from 1947-1948 is perhaps better termed a "consolidation" as it was a 25% pullback before the market continued to new heights. The market climbed up another 230% from 1949-1956 even as inflation rose to 7.9% in 1951 and the 10-year Treasury stayed around 2.5%. By 1953, inflation had slowed down.

The combination of high inflation and low Treasury Rates proved very beneficial for equity holders. The period was characterized by low unemployment (below 5% from 1942 on) and economic growth as the U.S. economy ran hot in the wake of WWII.

The Great Inflation Lie: The Fed Won't Stop Inflation

As recently as June, the Federal Reserve was projecting a PCE inflation rate of 3.4% for 2021. Three months later it hiked that projection up to 4.2% for 2021. One month after their meeting, PCE inflation was 5%.

Earlier this year, I highlighted what I termed as "The Great Inflation Lie". Either the Federal Reserve is incompetent with projections that aren't even in the ballpark of reality, or it is intentionally being misleading. When random average Joes are being surveyed and are more accurate than the Federal Reserve with their projections, something is wrong.

I do not believe the Federal Reserve is that incompetent, that they failed to see what everyone else in the country could see.

So why do both Government and the Fed want inflation to run very high?

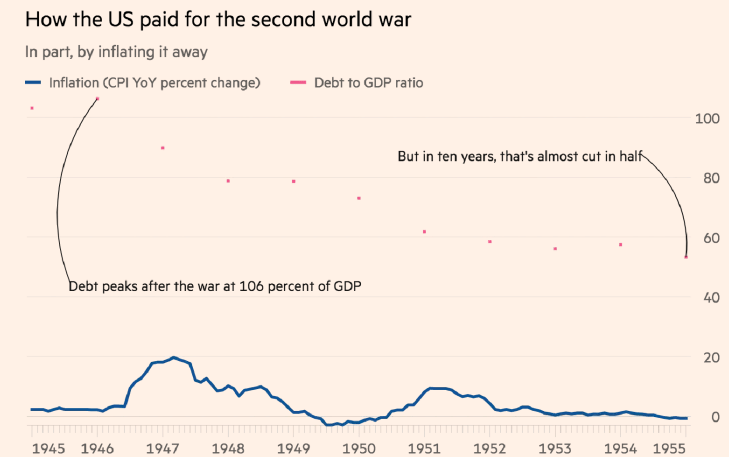

The U.S. Government has run up a ton of debt. As a percentage of GDP, the Federal debt is now over 120%. The cost of COVID alone was several times higher than the cost of WWII in today's dollar terms.

Politically this is a very unpopular issue to deal with because budget cuts and higher taxes aren't really popular with anyone. While some support for token moves might occasionally gain enough support to pass, comprehensive solutions aren't even seriously discussed.

To make matters worse, the U.S. Government has massive financial obligations coming up as Medicare and Social Security will both become much more dependent upon general tax funds as they fail to fund themselves.

So without meaningful budget cuts and/or meaningful tax increases likely off the table in a polarized country, how does the government pay off all that debt? It doesn't.

The last time the U.S. had debt/GDP of over 100% was in 1946. The U.S. Government had a massive debt of $269 billion. Just by reading that number, you know what happened. What is $269 billion to the U.S. Government today? That is only half of what the government spends on interest payments alone! $269 billion just isn't what it used to be, and that was intentional.

The U.S. never "paid" for WWII - it refinanced the debt, and through inflation, the significance of the debt dissipated quickly, even as the total debt grew.

A significant amount of inflation is the only solution that the U.S. Government has to manage its debts and obligations.

With debt levels far beyond the pale of productivity levels (i.e., embarrassing debt to GDP ratios), the U.S. and other developed economies are mathematically and factually unable to ever grow their way out of the debt hole they have been digging us into for years.

It is too late to fix all the past mismanagement. It is also impossible to force new generations to pay for debt accumulated by the older ones by taxing them to death and forcing them to be productive in the labor force well above the age of 75. Not only will it result in political unrest, but there are simply not enough young people to tax due to an aging population, and a wave of baby boomers retiring soon.

The only way to deal with this black hole is through inflation.

Conclusion

Don't be fooled by Fed Chair Powell's hawkish talk. After all, he has a hearing to keep his job coming up in January. Treasury yields are NOT pointing to a recession and/or deflation. They are telling us that liquidity will remain high and that the treasury market is not buying the hawkish story the Fed is selling.

We are seeing dynamics that the stock market has not witnessed for over 70 years. The inflation rate will remain above the 10-year Treasury rate for a sustained period of time, creating an environment of high inflation and relatively low-interest rates. Historically, this dynamic has been very beneficial for equity markets!

Right now, it is a fantastic time to be an investor and the worst time to be sitting on cash. Investors want to be exposed to equities that benefit from high inflation, while also benefiting from low treasury yields.

My strategy includes investing in:

Value dividend stocks: These are stocks that are valued based on earnings they have today and are paying out generous dividends. When cash is losing its earning power daily, you want cash now, not in a few years! Liberty All-Star Equity Fund (USA), yielding over 10%, is a fantastic CEF to gain broad exposure to the stock market that is overweight on "value" strategies.

Companies with Real Estate Assets: Companies with high levels of real assets, like REITs, will see ideal conditions. They will be able to borrow cheap thanks to low interest rates, while inflation will drive up rents and property values. Some of our picks include "Dividend Aristocrat" crowns yielding +5%, that are well-positioned to take advantage of these dynamics!

Economically sensitive stocks: The combination of low interest rates and rapid growth means that economically sensitive stocks will run hot. Default rates will remain relatively low as the burden of debt becomes less significant for borrowers, and the excess liquidity in the financial system ensures refinancing will be easy. "CLO" funds like Oxford Lane Capital (OXLC) yielding over 12% will thrive in this environment while producing a generous yield for investors.

Energy & Commodities: Energy frequently leads the inflation wave as we pointed out long ago we are entering a commodity supercycle. These companies will benefit from a combination of higher prices, while at the same time being able to access inexpensive debt thanks to low interest rates. And yes, you can get fantastic yield of +8% while investing in commodities. You don't have to worry about price fluctuations, exactly because you are getting paid extremely well to wait!

I am looking forward for the year 2022 to be a very strong year for equities. I am personally keeping as little cash as possible in my investment account, taking out what I need, and redeploying the rest of my dividends into income investments. The last thing anybody wants is a 6.8% inflation eroding the purchasing power of their hard-earned savings. Being invested in the right stocks which offer both high yield and growth helps you not only to protect your principal, but also increase your net worth in today's difficult environment.

It is critical that investors are aware of the major macroeconomic forces at play that are impacting the markets so that you can make informed decisions. I write "Market Outlooks", similar to the above which I share every Sunday with members of my investment community, to keep focus on the big picture as it evolves. This helps us make adjustments to our portfolio as needed, in a planned and methodical manner.

If you want full access to our Model Portfolio and our current Top Picks, feel free to join us for a 2-week free trial at High Dividend Opportunities.

We are the largest income investor and retiree community on Seeking Alpha with over 4800 members actively working together to make amazing retirements happen. With over 40 individual picks yielding +7%, you can supercharge your retirement portfolio right away.

We are currently holding a limited-time sale with 10% off your first year!

Markets: Investors hope the annual “Santa Claus rally” will lift stocks in the short week leading up to Christmas (the markets are closed on Friday). But with everything slowing down ahead of the holiday, trading will be thin, which could lead to more volatility.

World politics: Leftist Gabriel Boric, a 35-year-old former student protest leader, was elected president of Chile in a major ideological shift for the historically investor-friendly nation.

Turkey is run by a madman, Recep Tayyip Erdoğan. Like a Chicago Democratic Machine politician, he is consumed with one thing, power. He was first elected in 2014. . . .

When I saw Turkey’s real inflation rate, I was happy that the US dodged a bullet today. Build Back Better, along with lots of other policies being proposed by the radical Democratic Socialist Party in the US are inflationary. They also take away freedom.

Remember, inside every Democrat is a totalitarian dying to get out. Don’t believe me? Read what they are proposing in left wing NY State. Quarantine camps anyone? I remember when we called them concentration camps or gulags.

On Friday, senator stolen valor a.k.a. Democratic Senator Richard Blumenthal (CT) apologized and pleaded ignorance when it was exposed that he attended an event affiliated with the Communist Party USA the previous weekend. The entire story came and went last week without so much as a second of airtime from ABC, CBS, NBC, CNN, or MSNBC.

* * * * * * * *

Maybe Blumenthal would have known they were Communists had they made overt appeals for people to join their party. Oh, wait…

At the event, an organizer hit many of the Democratic Party’s talking points as he was pitching the Communist Party. “We invite you to join the Communist Party in this epic time as we make good trouble to uproot systemic racism, retool the war economy, tax the rich, address climate change, secure voting rights and create a new socialist system that puts people, peace and planet before profits,” Ben McManus proclaimed.

And another presenter said the quite part out loud and boasted about how socialism was the vehicle towards their political ends. “There’s more and more people talking now about socialism in this country as it becomes more and more clear that capitalism is not going to work for our future,” she said.

Remember that the next time a member of the liberal media claims socialism and communism are Republican boogiemen used to gin up fear.

Just think of the media as Democratic Party operatives with bylines, and the lack of television coverage makes perfect sense.

Evergreen: On Friday, senator stolen valor a.k.a. Democratic Senator Richard Blumenthal (CT) apologized and pleaded ignorance when it was exposed that he attended an event affiliated with the Communist Party USA the previous weekend. The entire story came and went last week without so much as a second of airtime from ABC, CBS, NBC, CNN, or MSNBC.

* * * * * * * *

Maybe Blumenthal would have known they were Communists had they made overt appeals for people to join their party. Oh, wait…

At the event, an organizer hit many of the Democratic Party’s talking points as he was pitching the Communist Party. “We invite you to join the Communist Party in this epic time as we make good trouble to uproot systemic racism, retool the war economy, tax the rich, address climate change, secure voting rights and create a new socialist system that puts people, peace and planet before profits,” Ben McManus proclaimed.

And another presenter said the quite part out loud and boasted about how socialism was the vehicle towards their political ends. “There’s more and more people talking now about socialism in this country as it becomes more and more clear that capitalism is not going to work for our future,” she said.

Remember that the next time a member of the liberal media claims socialism and communism are Republican boogiemen used to gin up fear.

Just think of the media as Democratic Party operatives with bylines, and the lack of television coverage makes perfect sense.

How Not to Resolve the Paradox of ToleranceNew Discourses

Education

The New Discourses Podcast with James Lindsay, Episode 17

Repressive Tolerance Series, Part 1 of 4

We live in a crazy world today that seems to have gone off the rails. That's because it is being driven by a broken logic, and, for all the flaws on the right, that broken logic is centered in the no-longer-tolerant left. The logic of the left today is overwhelmingly rooted in a single essay published in 1965 by the neo-Marxist philosopher Herbert Marcuse. That essay is "Repressive Tolerance." The thesis statement of this essay can be boiled down to "movements from the left must be extended tolerance, even when they are violent, while movements from the right must not be tolerated, including suppressing them by violence." This asymmetric ethic has been the heart and soul of left politics in the West since the 1960s, and we're living in the fruit of that catastrophe now.

To help people understand this vitally important and intrinsically totalitarian essay and its relevance to our present moment, James Lindsay walks the listener through Marcuse's "Repressive Tolerance" in a four-part lecture series. In this series, he reads the essay in full and attempts to make clear how it is the logic underlying the present moment. The goal is to explain the essay as Marcuse would have understood it, in his own context, and to show how his own logic has become dominant and the monster that he believed he was fighting.

In the first part, Lindsay begins by framing the Frankfurt School of Critical Theory to give background on Marcuse. He also explains that Marcuse seems to be attempting to give a solution to Karl Popper's famous "Paradox of Tolerance," which was provided as an aside in his 1945 book The Open Society and Its Enemies, which analyzed how fascism can arise and overtake liberal societies. Marcuse's answer to this conundrum is that a "discriminating tolerance," a "liberating tolerance," must be practiced that offers favoritism to the left and actively suppresses the right, as he defines them (from a perspective of Critical Theory). Join Lindsay as he contextualizes and then brings the first portion of this essay to life, and stay tuned for Parts 2, 3, and 4 to come!